With his sweeping victory today in Greece, Alexis Tspiras has led the far left to its only victory since his country’s return to democratic rule in 1974.![]()

In so doing, Tsipras (pictured above) and the socialist SYRIZA (the Coalition of the Radical Left, Συνασπισμός Ριζοσπαστικής Αριστεράς) have upended the political order in a country that, for more than four decades, shifted between the rule of political elites on both the center-right and the center-left, often hailing from two or three dozen well-connected families. Tsipras’s victory today is as much the defeat of that Greek political elite on both the left and right, which cumulatively share responsibility for irresponsible budget policies and widespread corruption in government.

More recently, they have also shared responsibility for the Greek bailout that ceded significant control over Greek fiscal policy to the ‘troika’ of the International Monetary Fund, the European Central Bank and the European Commission. Center-left prime minister George Papandreou (himself the son of a prime minister) accepted the first bailout in his term, between 2009 and 2011. Since 2012, a grand coalition headed by center-right prime minister Antonis Samaras and center-left deputy prime minister Evangelos Venizelos, have also accepted the increasingly onerous demands of the troika in exchange for the funding that has floated Greece’s treasury since the eurozone crisis of 2010.

* * * * *

RELATED: What to expect from Greece’s January 25 snap elections

* * * * *

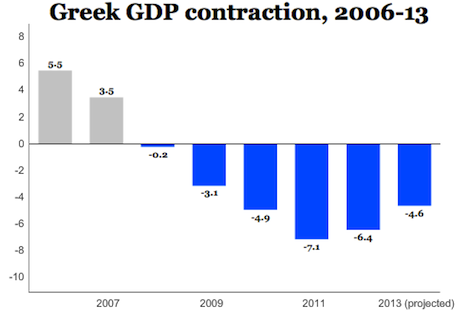

Tsipras, at age 40, emerged in the lead-up to the 2012 parliamentary elections, by consolidating support on the Greek left in his denunciations of the grinding course of austerity that accompanied Greece’s humiliating bailout. Then, Greece was only in its third consecutive year of recession and, remarkably, the unemployment rate was actually lower then (24.8%) than it is today (25.8%), with the country nominally back on the path to GDP growth.

But for all the smoke of the election campaign, and for all Tsipras’s fiery rhetoric, the reality is that Tsipras and SYRIZA have spent the past three years moderating their positions and preparing for the day when Tspiras would lead the next Greek government, which may prove more ‘pragmatic left’ than ‘radical left.’

In 2012, Tspiras was ambivalent (at best) about Greece’s eurozone membership. Today, however, Tspiras is adamant, along with a wide majority of the Greek electorate, that Greece must retain the single currency. Whereas SYRIZA once mused about defaulting on greek debt and ripping up the ‘memorandum’ of stipulations that governs the country’s two bailouts, which totals €240 billion, the party now pledges to renegotiate Greece’s debt burden with EU leaders in an orderly manner. Though Tspiras and other SYRIZA leaders are committed to reversing the grinding austerity of the past six years, they will seek to do so in the context of a balanced budget (as opposed to the 4% to 5% surplus that outgoing prime minister Antonis Samaras hoped to achieve).

Tsipras, in short, will govern more like a social democrat than a democratic socialist. As prime minister, with the full weight on government on his shoulders, Tspiras will be hard-pressed to deliver appreciable relief from six years of austerity, recession and unemployment. To devote more funding for public services and boost growth will require a very different skill set than the campaign oratory of the past three years. Continue reading EU should give Tsipras a chance to govern

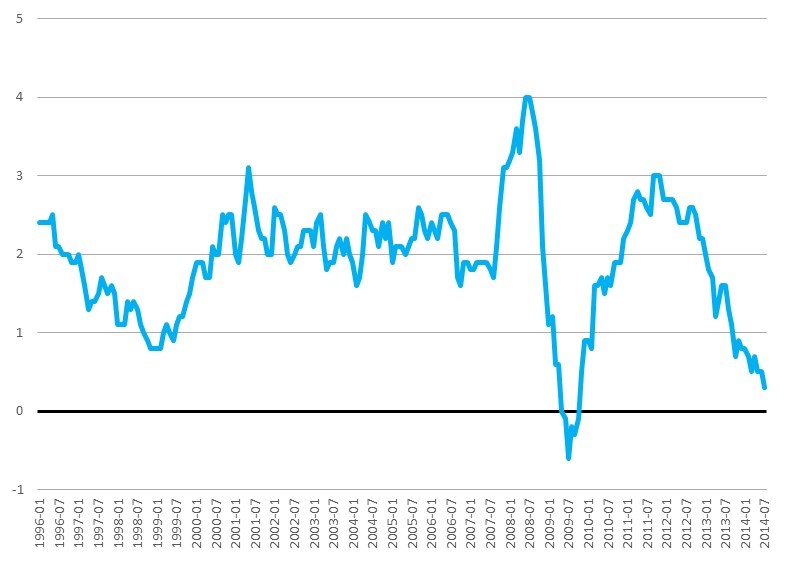

Draghi stressed that he understands the biggest risk to European Union’s economic recovery is deflation. He noted that the ECB is transitioning from a more passive approach to a much

Draghi stressed that he understands the biggest risk to European Union’s economic recovery is deflation. He noted that the ECB is transitioning from a more passive approach to a much