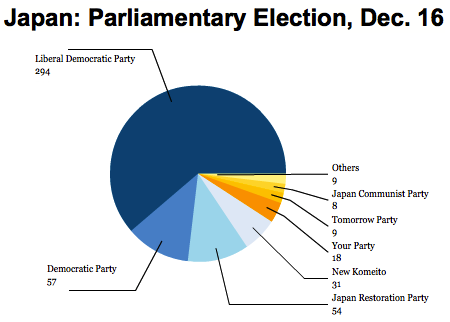

Over at Slate, Matthew Yglesias made the argument last week that the likely victory of former prime minister Shinzō Abe (安倍 晋三) and the return of the Liberal Democratic Party of Japan (LDP, or 自由民主党, Jiyū-Minshutō) to government after a three-year hiatus means that Japan might finally embark on a path of more expansionary monetary policy — namely, more quantitative easing and a higher inflation target.

With Japan apparently headed back into a recession — its fifth in 15 years — that strategy could be the surest way to boost the Japanese economy, but it’s a little naive to believe Abe can command enough political support, even with a landslide victory in Sunday’s election, to dictate monetary policy to the Bank of Japan.

Earlier in the campaign, Abe pledged to force the Bank of Japan to purchase construction bonds directly from the Japanese government (although, as Yglesias notes, Abe has already backed down from that pledge during the campaign). Abe needs the BOJ to buy those bonds in order to finance additional infrastructure spending, with the LDP calling for up to ¥200 trillion ($2.4 trillion) in public works over the next decade. Public spending is an old LDP favorite, but that staggering amount of spending could well pull Japan’s economy out of recession and deflation.

Abe has also pledged to appoint a new bank governor — the term of the current Bank of Japan governor Masaaki Shirakawa (白川 方明) ends in April 2013 after five years heading the BOJ — who agrees to set an annual inflation target of 2% or even 3%.

Abe’s push for expansionary fiscal and monetary policy comes as a bit of a 180-degree turn, given that the third and final government of the Democratic Party of Japan (DPJ, or 民主党, Minshutō) under prime minister Yoshihiko Noda (野田 佳彦) recently expended its last gasp of governing willpower to double Japan’s consumption tax from 5% to 10%, which is scheduled to begin in 2014.

It seems much likelier that Abe could implement a new round of fiscal expansion than strong-arm the Bank of Japan, which has an extraordinary amount of central bank independence — derived in part from the memory of hyperinflation that resulted after World War II when politicians controlled monetary policy decisions.

Noda (pictured above, right, with Abe) has attacked Abe’s platform as a dangerous intrusion on central bank independence and he has attacked the LDP plan for additional debt-financed spending as the same old LDP ‘baramaki’ (pork barrel) politics, especially given Japan’s debt-to-GDP ratio is already, by far, the world’s largest, at around 230%. Greece, by the way, has only a 160% ratio.

Japan has traditionally been able to carry such a high ratio because much of that debt is held by its citizens, who collective have one of the top savings rates in the industrialized world, but with $13.64 trillion in debt already on its public books, it’s not clear whether Japan could sustain public spending that would boost its debt-to-GDP ratio to nearly 300%.

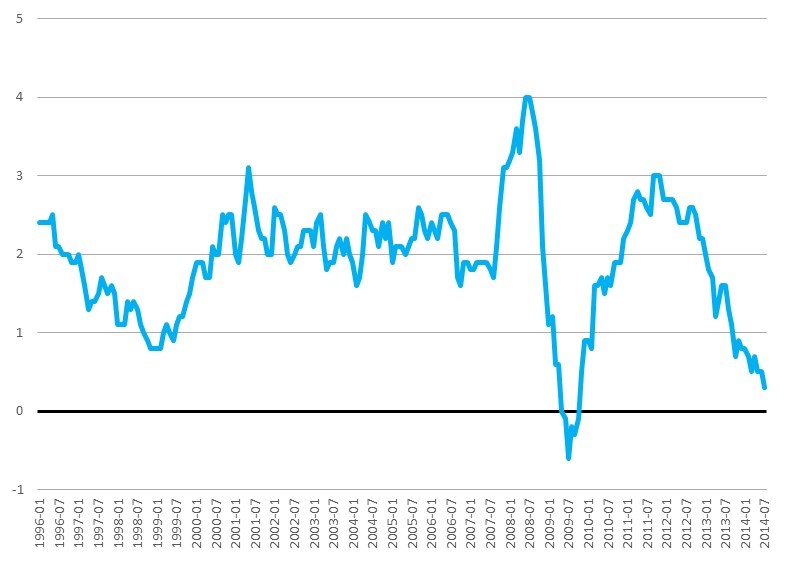

As Yglesias notes, the Bank of Japan has been criticized for nearly two decades for its policy to keep Japan’s inflation target at zero:

Back in 1999, Ben Bernanke condemned the self-induced paralysis of Japanese monetary policy made by flailing officials who claimed it was beyond their power to fix this. He called for “Rooseveltian resolve” on the part of Japan’s leaders to shake the bank out of its torpor. Paul Krugman, too, spent the late ’90s urging Japan to aim for more inflation, arguing that mucking around with the banking system was inadequate and weird delusions of respectability were holding policymakers back.

As Yglesias also notes, Europeans and Americans promptly forgot that advice when the 2008 financial crisis exploded budget deficits:

Suddenly, criticizing the Bank of Japan went out of style. America became Japan and simultaneously forgot what America used to think about Japan.

But perhaps the lesson that Yglesias is forgetting — and the lesson that the 2008 crisis taught Europeans and Americans — is that politics matters, and that politics can intrude on what might otherwise be a clear policy path, whether it’s ‘fiscal cliff’ negotiations in the United States or the ‘kick-the-can’ politics of eurozone bailouts.

Yglesias is also forgetting that Japan has politics, too. Continue reading Can Shinzō Abe boost Japan’s economy? →

Draghi stressed that he understands the biggest risk to European Union’s economic recovery is deflation. He noted that the ECB is transitioning from a more passive approach to a much more active ‘QE-style’ approach to the bank’s balance sheet — in part by moving last month to purchase private-sector bonds and asset-backed securities. Even if Draghi’s efforts still fall short of the kind of quantitative easing (e.g., outright asset purchases) that the Federal Reserve introduced to US monetary policy five years ago, Draghi committed himself to lifting the eurozone’s inflation from ‘its excessively low level’:

Draghi stressed that he understands the biggest risk to European Union’s economic recovery is deflation. He noted that the ECB is transitioning from a more passive approach to a much more active ‘QE-style’ approach to the bank’s balance sheet — in part by moving last month to purchase private-sector bonds and asset-backed securities. Even if Draghi’s efforts still fall short of the kind of quantitative easing (e.g., outright asset purchases) that the Federal Reserve introduced to US monetary policy five years ago, Draghi committed himself to lifting the eurozone’s inflation from ‘its excessively low level’: