With the failure of Greece’s parliament to elect a president after a third and final vote this morning, prime minister Antonis Samaras will dissolve the parliament and schedule early elections — most likely on January 25.![]()

It will be the first election since June 2012, when Samaras’s center-right New Democracy (Νέα Δημοκρατία) narrowly defeated the hard-left SYRIZA (the Coalition of the Radical Left — Συνασπισμός Ριζοσπαστικής Αριστεράς). According to just about every poll, SYRIZA holds a lead of between 3% and 7% against New Democracy.

Expect a tough Samaras-Tsipras fight for first place

Samaras is a wily and seasoned campaigner, and he will undoubtedly cast himself as the guardian of Greece’s long-term stability. On Monday morning, he was lashing out at ‘political terrorism,’ and warning that a SYRIZA victory would allow Greece’s sacrifices to go to waste. SYRIZA will face sustained criticism — some justified, some overblown — from just about every quarter in Europe that it and its leader, Alexis Tspiras, are dangerous ideologues whose policies could force Greece out of the eurozone in 2015. Already, publications like The Guardian are referring to Greece being ‘plunged into crisis.’ Expect the fear-mongering about the consequences of a SYRIZA victory to be on par with efforts by the British political establishment and business community in the fraught week leading up to the Scottish independence referendum. It’s by no means certain that SYRIZA’s narrow single-digit lead will survive that kind of onslaught.

The fight between SYRIZA and New Democracy is so important because the first-place finisher in the election will not only win the largest share of seats in the 300-member Hellenic Parliament (Βουλή των Ελλήνων), but also a 50-seat ‘bonus’ meant to provide the winning party with enough seats to form a working majority government. Over the next few days, it will be worth watching to see whether SYRIZA or New Democracy convince any other smaller parties to merge, because the marginal value of even a one-vote victory in Greek elections is so consequential.

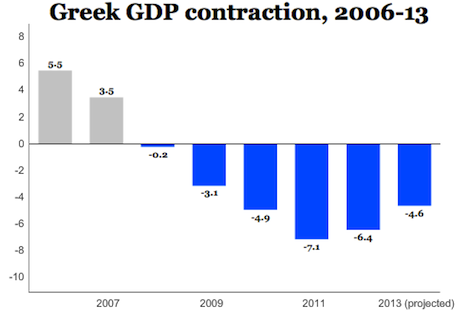

Since 2012, Greek economic conditions are slightly improved. Greece’s GDP is set to grow by between 1.0% and 1.4% in 2014, following six consecutive years of contraction, and there’s every reason to believe it will continue to expand in 2015. The government even attempted a reasonably successful bond sale in April, and Greece’s staggering unemployment rate is now just 25.7%, down from its high of 28%.

Nevertheless, the dual cuts of budget austerity and economic depression have, understandably perhaps, left the Greek electorate weary of renewing a mandate for austerity, and the uncertainty over the country’s political future has pushed 10-year bond yields to an unsustainable 8.5%.

Greece’s ‘bailout’ questions remain unsolved

Fueling that uncertainty is Greece’s planned exit from its bailout program in February 2015, just days after the election.

Starting in 2010, Greece received two bailouts, totaling €240 billion, from the ‘troika’ of the European Central Bank, the European Commission and the International Monetary Fund. Even assuming Greece continues the harsh austerity measures that its government has enacted since 2010, the next government will still need to find €12 billion in financing from the troika for 2015 and 2016, which wants to impose additional budgetary conditions, including wage cuts for some public employees.

Tspiras and SYRIZA have moderated their positions since 2012, but they still hope to reverse some of the austerity measures that the current government imposed, including an effort to privatize certain public-sector companies. Whereas the current government hopes to achieve primary budget surpluses of between 3% and 5% in the next two years, Tsipras merely wants Greece to balance its budget.

SYRIZA currently hopes that the European Union will write off half of the country’s €320 billion in debt and otherwise extend the repayment program of the rest of its debt for up to 60 years. Insofar as he realizes that Greek public debt load is unsustainable, Tsipras’s position is not so unrealistic for a country whose GDP in 2013 was around €198 billion. It’s easy to imagine that by forcing Europe’s hand, Tspiras could indeed win at least some form of bond haircut — the costs to Europe are relatively low to the uncertainty that would follow a new Greek financial crisis or its exit from the eurozone, which could snowball into a full-fledged eurozone financial crisis.

With Greece headed toward tough negotiations with EU and troika leaders in any outcome, voters might well be tempted to give Tsipras a shot at winning a better deal than Samaras or his predecessors have.

But Tspiras has been wrong before about extracting concessions from Europe — he cockily (and wrongly) predicted in 2013 that Greece would receive a bond haircut after the German federal elections. German chancellor Angela Merkel, in particular, is loathe to make any concessions to Tsipras, worrying that it would set a bad precedent for future member-states. Moreover, if Tsipras cancels Greece’s privatization program and increases social welfare spending, he’ll quickly find that he needs to raise much more than €12 billion for his first two years in office. That could force Tsipras to continue much of the prior government’s austerity measures, which could splinter SYRIZA.

The key figure in any Tsipras-led government negotiations with Europe will be George Stathakis, a leftist economist who is as measured and restrained in his rhetoric as Tsipras is fiery and impassioned. Stathakis recently met with London’s top bankers in a trip last month to the United Kingdom, and if SYRIZA wins elections, expect to see a lot of Stathakis in the days following the vote — if for no other reason than to prevent capital flight from a spooked business class.

A contest with implications for Europe

If he wins the January 25 polls, however, Tsipras will instantly become the leader of the anti-austerity movement across Europe, emboldening similar movements, such as Spain’s newly formed Podemos. It would make centrist leftists like Italian prime minister Matteo Renzi and French president François Hollande seem more moderate in their calls for pro-growth EU policies, and a Tsipras win might especially embolden Renzi, who boasts more domestic popularity than just about any EU leader today.

Accordingly, just as in 2012, expect to see key figures within the European Union indicate their support for Samaras (though not always in obvious ways). Merkel, European Commission president Jean-Claude Juncker, European Council president Donald Tusk and even British prime minister David Cameron will all be rooting for a Samaras victory, and may find subtle ways to influence the election.

Golden Dawn could win strongest victory yet,

potentially causing hung parliament

Polls currently show that the hard-right, paramilitary Golden Dawn (Χρυσή Αυγή) will likely remain the third-largest party in the parliament, notwithstanding the government’s 2013 crackdown on many of Golden Dawn’s leaders for inciting lethal violence. With an unapologetically militant anti-Roma, anti-immigrant and anti-Europe platform, Golden Dawn won 9.4% of the vote in May’s European parliamentary elections. If it repeats that result in January, it could potentially double the number of seats it holds in the Greek parliament.

No party, on either the center-right or center-left, is willing to align itself with Golden Dawn, so its success increases the chances of a hung parliament. That could mean a repeat of the 2012 scenario, when the May 2012 elections were so inconclusive that no one could form a government coalition, leading to the follow-up June 2012 elections. That would have the effect of prolonging even longer the EU post-bailout negotiations and add even more uncertainty to the Greek political drama.

Center-left in disarray

SYRIZA has been able to consolidate so much support among Greek leftists because it’s become the clearest brand for anti-austerity politics. That’s due, in no small part, to the splintering of the traditional Greek center-left over supporting the terms of the bailout.

Under its leader, former finance minister Evangelos Venizelos, PASOK (Panhellenic Socialist Movement – Πανελλήνιο Σοσιαλιστικό Κίνημα) has served as a genuinely loyal ally in Samaras’s coalition government, despite the party’s near-collapse as a force in Greek politics. As elections approach, its former leader, prime minister George Papandreou, has openly contemplated forming a new party, despite the fact that it was his father Andreas formed PASOK in 1974. A high-level PASOK split might prove fatal to Venizelos, depriving Samaras of a key partner in any future coalition.

To Potami (Το Ποτάμι), a high-minded centrist party formed in 2014 by television journalist Stavros Theodorakis, has at times shown potential of breaking out to attract wide support among the Greek electorate, but it fell far short of hopes in European elections in May.

Meanwhile, two small parties, the Independent Greeks (ANEL, Ανεξάρτητοι Έλληνες), an anti-austerity spinoff from New Democracy, and the Democratic Left (DIMAR, Δημοκρατική Αριστερά), a more moderate spinoff from SYRIZA, are in danger of falling short of the 3% parliamentary threshold altogether. After the June 2012 elections, the Democratic Left warily joined New Democracy and PASOK in government, but it left the coalition in June 2013 over the harsh nature of budget cuts. Its leader Fotis Kouvelis, once one of Greece’s most popular politicians, has indicated he would support a SYRIZA-led coalition.

Good job on short notice, Kevin! You didn’t have time to look up the revised GDP figures, though. 2012 was down 6.6%, 2013 down just 4%.

It seems likely the effect on the euro zone of a SYRIZA victory would be less than if something similar had happened a couple of years ago, right? Greek sovereign debt is owned overwhelmingly by institutions like the ECB that have no interest in running away. But the counterpart of that, I guess, is that the ECB is an even more formidable negotiating adversary.