Another late Sunday night in Brussels, another eurozone bailout plan for Cyprus — and it seems likely that the new deal between Cyprus president Nicos Anastasiades, and the ‘troika’ of the European Commission, the European Central Bank and the International Monetary Fund will endure much longer than last week’s disastrous plan, though capital controls to be implemented by the Republic of Cyprus’s government seem likely to lead to a backdoor eurozone exit for the nation of 1.15 million people.

![]()

![]()

The Cypriot-troika deal in brief

The deal will shield depositors with under €100,000 in savings from a ‘haircut’ levy, but depositors with funds over €100,000 now face an even more painful result –what amounts to a haircut for depositors and creditors alike at the troubled Bank of Cyprus (the largest Cypriot bank), and an even deeper haircut for Laiki’s depositors and creditors, who will take huge losses as Laiki is wound down. Laiki (also known as the Cyprus Popular Bank, the country’s second-largest bank) will be split into a ‘bad bank’ and a ‘good bank,’ the latter to be folded into the Bank of Cyprus.

All creditors at the Bank of Cyprus will see their interests restructured into a long-term equity interest and uninsured depositors will take an expected haircut of around 35% or 40%, with their deposits also held up for some time to come.

All the same, as Joseph Cotterill at FT Alphaville writes, the deal is better on two counts:

But there were two major injustices in the first Cyprus-Troika deal which made a mockery of the bail-in principle. Without debate, and upfront, it “taxed” depositors below the insured €100k limit alongside the uninsured. Then the tax was applied to either irrespective of bank. Why should small depositors in Barclays Nicosia or VTB Limassol take pain off large ones in Laiki or BoC, for instance. Well, finally, now we know. They shouldn’t have. The two unjust parts are gone.

Bonus points, I guess (if you’re a eurocrat), for structuring the deal in such a way that it can be implemented directly under Cyprus’s banking authority, so no need for another vote from the Cypriot parliament, which overwhelmingly rejected last week’s plan. That plan featured a 6.75% levy on all depositors with savings under €100,000 in any Cypriot bank. The parliamentary run-around, however, will only fuel the ‘democratic deficit’ hand-wringers throughout the European Union and breed resentment inside Cyprus and beyond.

The worst of the Irish and Icelandic precedents

Though the deal is ostensibly narrowed to focus on Cyprus’s two largest banks, and it’s better than last week’s plan, the deal essentially features the worst elements of the Irish and Icelandic examples.

Like Iceland, some of the Cypriot banking sector will be allowed to fail — Laiki’s uninsured depositors are out of luck, no matter whether they are Russian or Cypriot or whatever. That’s exactly how Iceland approached its banking sector failure.

But unlike Iceland, Cyprus does not control its own monetary policy, so it won’t be able to devalue its currency and take the kind of independent monetary policy steps to rebalance its economy in the way that Iceland has. Though Iceland is no longer the financial center it was before 2008, it has returned to GDP growth (around 3% in 2011 and 2.5% in 2012) and features relatively low unemployment — just 5.3% as of November 2012. In contrast, Cyprus remains trapped in the ECB monetary policy straitjacket.

But like Ireland, the rest of the Cypriot banking sector will be essentially nationalized by the Cypriot government, with a European bailout that is likely to require additional bailout assistance and will come with increasingly stringent austerity measures that Cyprus’s government will be forced to take that will invariably depress its own GDP growth. No one’s optimistic about Cyprus — it seems fated to suffer a fierce GDP contraction and a massive uptick in unemployment, joining Greece and Spain as one of the eurozone’s most troubled economies, no thanks to the Eurogroup’s clumsy policymaking.

Self-inflicted wounds to the European project

It’s worth repeating that the damage from the first Cyprus plan remains and cannot easily be reversed — Cyprus’s banking sector has now been decimated, probably permanently. As one unsentimental Moscow economist put it, Cyprus’s beaches-and-banks economy is now just beaches. The best hope for Cyprus’s economy is the rapid development of natural gas deposits that could bost its economy back after what will likely be a double-digit recession. But the ultimate scope and richness of those deposits are still unknown, and there’s no assurance that natural gas will be the country’s economic savior.

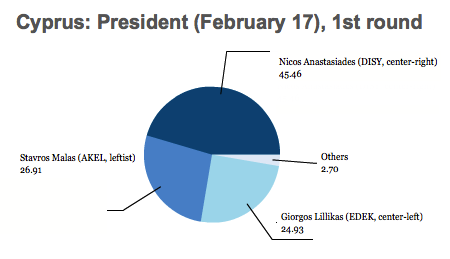

Brussels has so thoroughly undermined Anastasiades that he allegedly threatened to resign Sunday at one point, so it’s not clear how much legitimacy he’ll have in the next four years and 49 weeks of his five-year term, especially given that his own center-right party Democratic Rally (DISY, Δημοκρατικός Συναγερμός or Dimokratikós Sinayermós) controls just 20 of the 56 seats in the Cypriot House of Representatives (Βουλή των Αντιπροσώπων).

In addition to the obvious ammunition that eurozone leaders have handed to euroskeptics, no one in Spain or Italy or Slovakia or Latvia should be feeling very good these days about keeping their money in national banks, deposit insurance or not. Already today, Jeroen Dijsselbloem, the newly elected president of the Eurogroup of eurozone finance ministers (pictured above with IMF managing director Christine Lagarde), has released a statement walking back earlier comments that appeared to hail the Cypriot bailout as a precedent for future deals.

It’s been a horrible start for Dijsselbloem, who succeeded Luxembourg prime minister Jean-Claude Juncker — Juncker has already (very gingerly) criticized the Eurogroup’s post-Juncker approach to Cyprus, and it’s hard to believe that Juncker would have made some of the more glaring errors that Dijsselbloem has made — unlike Juncker, who was Luxembourg’s finance minister from 1989 to 2009 and has been prime minister since 1995, Dijsselbloem has served as the Dutch finance minister for barely over four months. It’s starting to look like the decision to appoint Dijsselbloem as a sort of compromise Eurogroup president (he’s a pro-growth member of the Dutch Labor Party who’s implementing an austerity regime in an otherwise budget-cutting government led by center-right prime minister Mark Rutte) may have been a poor one.

Capital controls are a backdoor Cypriot eurozone exit

While it’s far from an original observation — more sophisticated financial commentators and economists have made the same point — the biggest takeaway from the weekend is that Cyprus has essentially been booted out of the eurozone, in large part due to the capitol controls that Cyprus looks set to enact tomorrow when banks in the country reopen — here’s a short summary of the menu of options from Yiannis Mouzakis, based on the capital control bill that Cyprus’s parliament passed over the weekend. There’s optimism that the controls will be ‘very temporary,’ and will be somewhat lighter than originally feared, but it’s worth noting that Iceland’s controls are still in place even today, over four years after their imposition in late 2008.

The inescapable conclusion is that a ‘Cypriot euro’ is no longer the same thing as a euro throughout the rest of the eurozone.

As former banker Frances Coppola wrote over the weekend, the imposition of capital controls transforms Cyprus into something far short of an equal member of the eurozone:

Once full capital controls are imposed, a Euro in Cyprus will no longer be the same as a Euro anywhere else in the Euro area. It cannot leave the island. The Cyprus Euro will in effect be a new domestic currency. The imposition of capital controls in Cyprus is therefore the end of the single currency in its present form. Continue reading Cypriot-‘troika’ deal means that Cyprus is leaving eurozone in all but name